Alexander Shemetev (copyright protection),

Saint-Petersburg

For further questions, please, contact me at:

Anticrisis2010@mail.ru

![Alexander Shemetev's photo [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/alex123.jpg)

Abstract: The paper is devoted to the comprehensive financial analysis. Much attention is paid to its providing in the Russian context.

Alexander Shemetev, the author of this paper, provides a series of methods and models developed by him like: rapid matrix analysis of financial, operational-marketing and investment cycles functioning inside companies; models of comprehensive analysis of financial stability; method for weighted average cost of debt capital estimation; method company"s financial analysis based on payback period term analysis; comprehensive liquidity analysis ratios - these are the described here complex methods developed by Alexander Shemetev.

Also Alexander Shemetev describes the other concepts of comprehensive financial analysis and its elements in a simple form so that a wide audience of readers could easily understand the materials of this paper. It is also described how to analyze Russian companies in the Russian context through the prism of optimization transformations of financial statements. All the necessary financial ratios are represented in complex matrix systems by the author. All the difficult aspects of financial analysis are explained in simple schemes.

Keywords: comprehensive financial analysis; rating analysis; rapid analysis; common financial analysis; WACC analysis; financial sustainability analysis; financial ratios analysis; liquidity analysis; financial results analysis; financial efficiency analysis; business profitability and business-activity analysis; Alexander Shemetev"s models for financial analysis.

Section I. A comprehensive financial analysis of Russian companies on financial and economic indicators and their systematization: Alexander Shemetev"s models

A comprehensive financial analysis in Russia - is a relatively new concept. 15-20 years ago, under this analysis was understood primarily an economic analysis. Today, the topic is growing rapidly. A comprehensive financial analysis should help all directors and owners of companies to make their work more effective. It's no secret, that the state of affairs in a company is not transparent for senior management. And what if it comes not on its own, but about somebody else"s other company? People have adopted the practice in Russia to bifurcate or even sometimes to trifurcate (from the word "three") the reporting of company"s activities, sharing, by thus, managerial accounting, financial accounting and just accounting (for the concerned "legislative" (read: "tax") bodies). In this situation, rating the company from a position of a third party is difficult, and it similar to how when we try to see what is inside of some office space on the first floor where the entrance is closed, where there are no signs, except Company Limited "New Time", and where even the windows are mirrors - so nothing can be seen behind them .... Thus, the financial analysis of the company - this is not the easiest thing .... And it is the basis of any strategy and any company activities.

Dear reader, please, consider: how you can manage a company without knowing the exact state of affairs inside? How can you build a development plan on the market, if you do not know the state of competition?

In this chapter the author describes an integrated analysis algorithm of the company. And then you and I let us to investigate the details: we will conduct a comprehensive financial analysis of various aspects in a firm, such as marketing, management, risks, and so on. Financial analysis - is not a "magic wand" that will allow you to develop a strategy for your company simply by waving your hand. Financial analysis - it is rather a tool. And, like any tool, it will work just as much as much skills you will be able to use, and it will depend on how well you use them! And if you do not use it - then it will be done, and, probably, already is done by your competitors who will then take an advantage in the foreseeable future to push your company down to the "roadside" of the market occupied by your company. And then you will, probably, all have to start again .... Restarting the business from naught or, and that is much worse, from big debts is neither fun, nor "cheap", especially in Russia. You will have to Re-search for money, Re-search for capital .... At the same time you will need to develop a new business idea .... You will need to Find a qualified personnel .... That, in fact, is very difficult .... Then you will have to look for customer base and over and over again to fight with the competition..... Isn"t it simpler to keep the market from the very beginning, so that your company is to be "entrenched" in it forever? Isn"t it simpler to make your company sufficient it could be useful for you and your children and your grandchildren and so on?

You will be hard to keep the capital with no financial analysis, and it doesn"t matter how successful is your company now at the moment. You should remember that about 30 years ago the world lost one of the biggest investment network, which was run under the commandment of one of the richest people in the world, Mr. Adnan Khashoggi, a citizen of Saudi Arabia and a number of countries. His cartel developed itself rapidly in his time: he had the usual practice of personal selling of any goods at retail, when he, a mining engineer by education, once decided to do business in earnest, and he did.... Within the next 20 years he owned the factories, steamships, oil derricks, auto concerns (even such societies as Rolls Royce, Fiat, Chrysler, and so on depended on him much....), ...... And also he was suspected in the possession of the world's major shadow networks owner, including the network of wholesale selling the weapons....

Before to divorce his wife, Thoraya, which required him to pay her $ 2.5 billion in compensation for their marriage, he was considered by many global ratings as one of the richest person on the planet, with the capital, according to unofficial data, surpassed $ 70 billion (this is in the early 1980s, and it was approximately the same as to possess now $ 200 billion). He did not have a proper financial analysis, and he did not do it in the complex, and his business began to be pursued by a set of setbacks. By the early 90s, he almost became a real "multi-billionaire in minus", this is when a person has a wealth over a billion dollars, and it is with a minus sign (ie, loans)..... And then he sold his houses, stopped his "usual" way of life to which he had spent circa 600 thousand dollars a day, he has sold his aircraft, yachts, the companies .... - And then he stayed in his big mansion with a fleet of cars and thousands of business suits ....

There are many similar examples in the world. Financial analysis, of course, is designed to answer the main question: "How to earn money for a specific company?". The second major issue on which it is intended to answer - is: "How to save the capital?". In fact, the art of business consists of three pillars, which can be expressed in search of answers to these questions: "How to earn capital?" "How to save capital?" "How to invest capital to extend the life of business?". The same algorithm works for the ruining of the firm. Let's look at the sequence in which the company withdraws from the market: First, the company can"t find the answer to the last question: "How to invest the capital to extend the life of business?" - And it inhibits the investment cycle of the business. After about a year or two, manufactured by company products become more and more obsolete, distribution channels - become more and more weak, there may appear a lot of "legs" at the enterprise, and day after day there are no new investment projects....- That is when the company, due to the presence of the above mentioned algorithm, starts to face with the second question: "How to preserve capital?" - Literally, it can be translated as: "We started having problems with production and with sales!" - And this is a crisis of the so-called operational or operation in the production cycle of a business-system! All this over a period of time results in that inventories" glut grows, not many want to buy production, and the money are needed...and really very much!

As a result, the company begins to "intercept" the money (here and there - no matter where) to cover the debts arising from temporary.... Here, there is no money to pay salaries - but it is for now, temporarily, in a month we will wriggle out and close the debts, - the companies motivate their behavior. And then the crisis of investment and operating cycles increasingly making its presence felt.... The business affairs of a company go from bad to worse....and the company is beginning to take out loans to cover other, the earlier loans and...a company falls into the bondage of financial leverage in the Russian context .... Then the debt grows, the capabilities fall to cover it - it is the company"s leaving the market that is associated with the crisis of the financial cycle of the company. This is how the most companies become bankrupt in the Russian context! I and you do not consider a fake or deliberate bankruptcy - we consider only "real" bankruptcy associated with this company and its present activities!

![Company's functioning scheme [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s3.jpg)

![Company's functioning scheme [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s1.jpg)

There is the only one way to prevent all this - by carrying out a comprehensive financial analysis and, more importantly, correctly interpreting the results.... You, probably, ask me now: "What kinds of complex financial analysis exist?" - There are two kinds of a comprehensive financial analysis: 1 - These are not complex types (rapid analysis and rating approach) and 2 - truly comprehensive ones: - these are: 1 - comprehensive financial analysis and 2 - anti-crisis financial analysis. Let us consider them in more detail!

Let's start with the rating approach. Financial analysis - this is quite a complicated thing, - especially when it comes to specific types of companies, such as banks, which are discussed - a bit later. So, suppose you need to conduct a comprehensive financial analysis and, moreover, it is necessary to be carried out all the time. How, then, it should be good to resort by using third-party analysts, who are engaged in it professionally?! In about 10 years ago in Russia it was mostly used only a comprehensive financial analysis and each organization did it within itself, that is, independently from third parties; as well as each organization assessed its competitors. This was justified, because who is thee who can analyze competitive positions and sales in an industry a selected region of presence better than the companies themselves, the companies who work there and who know the major competitors "in face." Today Russia is increasingly resorted by the third-party-financial-analysts-usage, by the analysts who themselves, in most cases, use the rating approach in evaluating companies. The rating approach is especially popular abroad. Rating approach would tend to rank all companies in a seleted industry, or the whole market as a whole by any key figure, or a small group if figures. We consider it fashionable to take such indicators as revenue, operating profit, asset value, net asset value (this is assets minus liabilities). In the west people take these same indicators, plus a couple of fashionable indicators they have, such as number of workers, the payroll, company"s stock price. The rating model has its advantages. It is easy to use, and it allows you to quickly monitor the market, to assess a company as a whole. And, nevertheless, it has some drawbacks. Among these shortcomings can be called too cursory glance at a company and at an industry, the difficulty of forecasting the negative trends for companies, particularly, in the long run, the complexity of the application for the purpose of anti-crisis management, the impossibility of taking into account the discrepancies" facts of official and management reporting in the Russian context, and so on. Thus, the rating approach is appropriate if you want to get a quick overview of some industries and companies that are working there. Apply the rating approach is simple. Ranking methods are of two types: linear and discriminant .

Linear models of the rating analysis are suggested to do the rating calculation by the only one indicator using, most often, by total assets" sum.

For more visual perception, let us consider the example of making the rating on the linear model. Let"s have 10 companies taken: # 1, # 2, # 3, # 4, # 5, # 6, # 7, # 8, # 9, # 10, - with total revenues at 61, 56, 48, 41, 32, 28, 22 , 19, 15, 12 million rubles on the profit and loss accounts respectively. It is known that it covers approximately 80% of occupied by the companies market segment in their region. This is the rating (the company number 1 takes place 1, ? 2 - the second place, and so on). That is, to create the rankings, we need to simply rank the amount of indicators for specified companies. Why, then, the model is called linear if involves ranking? The fact that the higher is the volume of a ranked indicator, - in our example, the indicator is revenue, - so therefore the higher is the company's rating compared with the previous ranking position, so, therefore, this implies greater stability of company and the greater business success at the market.

Discriminant models make the same ranking, and here the ranking rate indicator is derived from real-world performances. The formula for the ranking rate indicator in this model will be next.

![The formula for the ranking rate indicator in this model will be next. [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f0.jpg) (0)

(0)

Where: D - resultant discriminant rating index ; A - shows which value is not included in the rating factors, for example, this figure may reflect the market shares of other, unaccounted in making the ranking companies, or it may reflect the current market factors; a, b, c and so on - are the very discriminants, which show us how one selected indicator is more important than another one in the model, and also it demonstrates how well it is more important; x1, x2, x3, ..., Xn - these are financial figures involved in the ranking.

For more visual perception, let's look at the same example, with some adjustments. Let the importance of revenue in the financial performance of a company is 25%; the importance rate of the amount of equity - 75%; and the significance of net profit - 25%. All data for all companies is performed in the table.

![Table: Summary of companies’ ranking, mln. rub. [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/t1.jpg)

Let us, for example, calculate the total ranking score for the company number 1 at the market.

Where: 55 - is a conditional indicator, in which will now be ranked all the companies under specified conditions. A = 0, because other conditions for the discriminants are not specified in prior for this ranking. Usually, the sum of the coefficients of discrimination tends to 100% or to 1 in discriminant method of ranking, although it all depends on the specific methods used, and that to which factors the method is attached. Similarly, the data is considered for all the other companies. The calculation results for all companies are listed in the table below.

![Table: Ranking of companies ranked by discriminant approach [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/t2.jpg)

So, it turns out that the company number 5 ranked first in the ranking, ? 3 - is the second and so on.

That's how the linear and discriminant ratings are to be done for companies in the ranking approach. As it can be seen, the method is quite simple. It can be applied easily to all types of companies, including, without specialists" attraction, and for all the industries. Even people, - who had never seen such a specific type of companies" reporting, like banks" reporting, - should be easy to make their own ratings in all banks of interest on various parameters and decide for themselves - which one is stable, and which one - no.

However, this approach represents a number of significant disadvantages associated with non-integrated and non-systematic approach to financial analysis. As a consequence, significant "anxiety indicators" of deterioration or improvement in the performance of individual companies can"t be seen. Even in Europe, - where reporting is very transparent, - the application of the rating approach has contributed to the current economic and financial crisis; as this approach was not effectively able to show the actual trends of development of individual business-systems.

Russia has always had a place to be a difference in managerial and financial accounting, which greatly reduces the effectiveness of the approach based on the rating, applied for the Russian reality.

Another drawback of the rating approach is that it is fashionable to carry out an assessment from third parties, who are not so obviously interested to find out everything objectively in the internal environment of companies inside a selected industry, as interested in it themselves guide and owners of companies, which are present in a selected market segment.

Some authors have suggested the construction of scoring and rating systems of the financial analysis of companies, based on the discriminant company size. The concept of discriminant size of a company was introduced to science by Sofia Balkaen (Belgium), being one of the points of her doctoral dissertation defense in 2009 (study 1982 - 2009.). Discriminant company size (DCS) - is the natural logarithm of total assets of a company:

![Discriminant company size (DCS) – is the natural logarithm of total assets of a company: [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f01.jpg) (0.1)

(0.1)

Where: ln - is the natural logarithm (logarithm of the "e") of the amount of assets, denominated in comparable monetary value with other companies under comparison. For Russia it is thousands, millions or billion rubles. For comparison with international companies - these are thousands, millions or billions $. All this will have little value if the company compared to the same value, for example, all in rubles.

Discriminant company size can be calculated from the amount of assets from the proceeds, net assets, equity and so on.

Now, let's consider the second kind of not a comprehensive financial analysis, a rapid analysis (or express-analysis). Express-analysis - is an analysis of a company, on the one hand - deep, on the other hand, - very fast even with a simple calculator. Sometimes the analyst has no time and resources at hand to conduct a comprehensive analysis of a company, and he or she wants to know what is happening there, inside - really want.... In this case, the express-approach can help you, dear reader, a lot! You can conduct a rapid analysis based on a number of different approaches. Here we consider some approaches, including an approach based upon a model of Dupont, the model we"ll begin consideration of a small part of this chapter devoted to rapid analysis. Then you and I look at some more companys" rapid analysis methods and then proceed to evaluate integrated approaches. So let's start .

I) Coefficient model of company"s express-diagnostics.

1) Rapid analysis for firm"s anti-crisis management

(The method is based on the Dupont model under the supervision of Professor

A.V. Grebenkin and others)

So, what documents you and me need at express-analysis of a company based on this model? Well, first of all, we need a balance sheet. Secondly - the profit and loss account. That's enough. Other sources the analysis needs from you are, at least, a pencil, notepad and calculator, you can also have the personal computer in any form.

After analyzing some company on the basis of this model, you can calculate the feasibility of new venture projects and innovations; you can view what is the impact on the dynamics of return on equity there is in the firm and find out what causes can lead a company to a crisis, to evaluate what to do next to make a business-system little susceptible to a crisis of external and internal environment of an organization.

Dupont model derived from the very simple formula: return on equity. Let's analyze it:

![Dupont model derived from the very simple formula: return on equity. Let's analyze it: [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f1.jpg) (1)

(1)

So, 4 coefficients (C) are received in this model (the formulas # 2-5):

C1 = NP/OC(Eq);

C2 = NP/Rev;

C3 = Rev/A;

C4 = A/OC(Eq)

If you have difficulties with the identification of these ratios and of the value of the components that income in these ratios, or you would like to strengthen your knowledge about them, please, dear reader, look at the footnotes to these factors at the bottom of the page.

Note that before you consider the above factors, you would have to calculate another measure: the proportion of accounts receivables in the balance sheet value of the company, which is calculated by the formula (6):

C5 = AR / A.

The growth of the negative trend indicator shows the concentration of problems in the financial cycle of operation of a business. It is very likely may indicate problems in the operating and investment cycles of functioning of the company.

This, as you remember, is an "alarming beacon," which shows that the company may be something quite different from normal. If the value of this coefficient is insignificant - it should not be taken seriously about the above-mentioned crisis probability.

The real danger begins when the values of this ratio is significant compare to the book value of the company, and when it itself begins to grow rapidly.

There is the so-called theory of a catastrophic development of all business systems. This concept maintains that a company is doomed to the elimination over time, while the above figure can serve an alarming beacon pointing to the fact that the development of the company is a question of catastrophic model, since this indicator indicates the possibility of significant problems for the company related with liquidity.

Now let's look at a small outline of what to do when the company"s functioning reveals problems based on our analysis of this model.

![Now let's look at a small outline of what to do when the company’s functioning reveals problems based on our analysis of this model. [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s4.jpg)

Now, for more visual perception of Express-diagnosis model based on the model of Dupont, let us, my dear reader, consider an example.

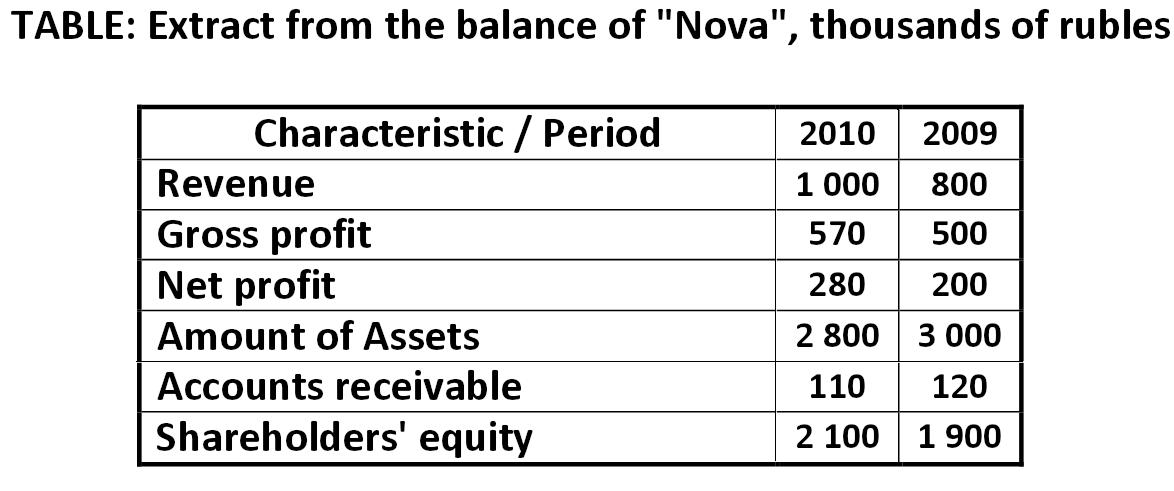

Example: Express-diagnostics and the development of anti-crisis strategy of firm based on the model of Dupont

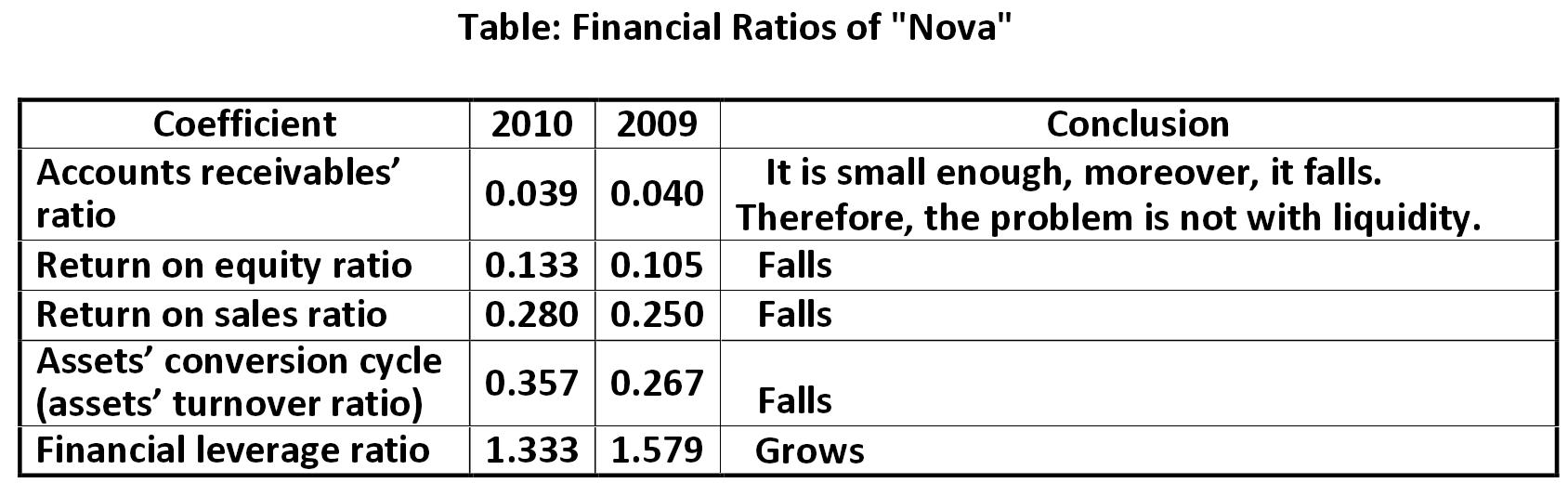

Let us now consider some important indicators of a conventional company "Nova" at the market, which are presented in the table below:

Data for the calculation of the five ratios and related with them factors is listed in the table below.

Thus, we can recommend the following to the "Nova" company, on the basis of express - diagnosis:

1) Company needs to improve the management of cash flows. This requires a more complex work with debtors and creditors, as well as the following recommendations are necessary;

2) Company needs for new products and entering new markets;

3) Company needs for new technologies;

4) Company needs to improve the quality of management of the organization at the highest level;

5) It is required a detailed plan for dealing with the crisis of external and internal environment;

6) Company needs to search for partners and investors, so that in case of crisis to get a subordinated loan from them or to merge with them to avoid the possibility of absorption;

7) Company needs to search for illiquid assets and to sell them;

8) It is necessary to reduce costs and expenses;

9) It is required a shift in marketing.

2) Coefficiental indicators" system for rapid diagnosis of the financial condition of the company both internally and externally on the basis of a systematic approach

I want to offer you another coefficiental model developed by the author. It is to assess the company's financial, operational, marketing and investment cycles. The model allows you to see what to do with company"s management.

As you may remember, the crisis in the company always starts in the investment cycle, then it moves into the operational (production) and marketing cycle, and, after all, the crisis turns in the financial cycle, when there start the problems with lack of money, liquidity, solvency, which ultimately finishes such company ... and

if you, my dear reader, is in an urgent need to find out which cycles of a single company have their problems and what are these problems - you can use the model, developed by Alexander Shemetev, to estimate this. Carefully read the following scheme to understand and remember the algorithm better:

![if you, my dear reader, is in an urgent need to find out which cycles of a single company have their problems and what are these problems – you can use the model, developed by Alexander Shemetev, to estimate this. Carefully read the following scheme to understand and remember the algorithm better: [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s5.jpg)

It should immediately be noted that the rate of NP / ((LTL / n)) in long-term priorities of the financial cycle should not be written more than 1.2, even if it is so in fact, for example, 12. This is because the fact the use of short-term loans by a company does not ensure the stability of the financial and other cycles. If the indicator is divided by 0, that is, there is no long-term debt, and then you should just put a 1.2 into this graph.

In general, this model aims to identify the specific activities of your company. It does not say what is good and what is bad. It does not build some kind of "ideal company" to compare your with it - no. It is simply designed to reveal the specifics of your company and, thus, it seeks to answer the question "What should thou do?", Omitting the scope of all other matters. This is not a model of "Who's to blame?" - it is a model of "What to do?" And "Where to oar in order to bypass the whirlpools?". You know, there is a Japanese proverb: "Never go to sea on a boat without oars." "Oars" - it is a financial analysis: rapid or general. Where to swim - it is you to decide, my dear reader, that is, in this situation you are like a captain or navigator. The author's recommendation is to use the latest navigation systems and maps (of reefs, depths, underwater currents and so on), as well as instructions for the use of modern navigation systems!

Maybe your company has a critical shortage of liquidity - and it is a key to the success of your business-activities. And this, however, can say that there are urgent problems in the financial cycle of the company, if an indicator does not show the norm and, therefore, you need to make every effort to minimize risk in this cycle, otherwise it can happen the negative outlook of development "by default". By default, if nothing is done - the company's activities are in the framework of crisis, when the coefficients-indicators do not correspond with each other. Then what kind of indicator is not corresponded so, it indicates in which direction to build an anti-crisis strategy. In order to analyze the "weak points" for your company, you can use proposed by the author of this paper matrix. The following footnote symbols are used in the scheme .

Do you want to know what is it in case "by default"? By default, the author proposes a visual model of prediction of risks" concentration in the business-system.

Now, let's look at the methodology in more detail. Horizontal bars indicate the financial, operational + marketing and investment cycles. The arrows indicate that rates are needed to be looked at the dynamics, at least for a year.

The general policy recommendations are written in the "Clouds" or each case in the company. Vertical bars indicate priorities: long-term, medium-and short-term.

Failures in the short-term priority indicators for all three cycles are the most critical, as they are capable to stop the development of this cycle, which can very substantially harm the company. Now, let's consider the critical factors for each cycle in more detail.

![This is a critical factor of the financial cycle [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f7.jpg) - This is a critical factor of the financial cycle (7)

- This is a critical factor of the financial cycle (7)

In the Russian accounting not all the payments for liabilities can be distributed before the NP forming (this will be discussed later). At the same time, even if it would be so, this indicator would nevertheless reveal the complex risks in the financial cycle and the needs to work with those risks.

If the net profit for the period is missing (an indicator of less than 1)! - This may mean shortages to cover short-term credit liabilities for this and subsequent periods; it indicates the likely presence of a problem of risk of a catastrophic failure in the functioning of a business-system by causing a lost in the ability of a fully self-finance: temporarily or permanently.

In this case, companies need to start immediately work with their creditors on possible variations of the payment schemes of debt (even if a company has a presence in the excess funds to cover them). Companies should look for potential and actual possibilities of TL repayment (TL - borrowed funds). Companies need to seek out and sell illiquid assets from turnover. Companies also need to find a subordinated investor or partner, a few more, if necessary, to obtain a subordinated loan (from this name we call such partner), or to merge with it, to avoid absorption or elimination. The company's goal is to find ways to close the debt "holes" in the budget to immediately proceed then to eliminate the problems in operational and marketing cycles.

![– This is a critical indicator of risk concentrations of two cycles [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f8.jpg) - This is a critical indicator of risk concentrations of two cycles (8)

- This is a critical indicator of risk concentrations of two cycles (8)

These are the operational (production) and the most important for profit generation - marketing.

If the net profit for the period is missing, and, in contrast to the previous index, - logically (an indicator is less than 1)!, It means that something is wrong with the production and marketing of the company. Either there is the crisis of overstocking, or obsolete technology of production which requires too much storage resources, or the finished product is not particularly taken by customers, or the production process is built irrationally itself, or advertising of the company is limping, .... Or there is something else.

All of the above can be summarized as follows. In short, this indicator is less than 1 means that the company has serious problems both on the X-Z-axis and on the A-C-axis of production and marketing functions of the curve.

Next, the author of this paper will consider you the scheme, which shows the structure of company"s goods and commodities on their perception by consumer through the prism of XYZ and ABC analysis.

Scheme: Structure of the goods sold ranged by the class of goods linked with their perception by the consumer

![Scheme: Structure of the goods sold ranged by the class of goods linked with their perception by the consumer [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s7.jpg)

Now, let's discuss this scheme in more detail. It's no secret that the production of the company depends directly on marketing. After all, if you have nothing to sell, then, consequently, there is nothing to produce for a company!

Marketing, and, consequently, the production cycle crisis is the measure of oversupply, of not the rational organization of the production process. On average, net profit for the period should be able to override the value of inventories and costs. Otherwise it means either that the company has significant problems with overstocking, or that the company wasted cumbersome production process in relation to the organization of marketing.

Cumbersome manufacturing process must meet an adequate consumption of the product produced by the company. If not, then the value of the net profit is not logically enough to cover the value of inventories and expenses during the same period of time. Therefore, there is an urgent need to change something in the company: reorganize production lines, get rid of items B and C in the range of products and switch the group A.

The method of statistical analysis of the market should get rid of the errors of calculation, to lead the company from high-risk marketing area or, worse, catastrophic marketing area to the area of an ideal marketing organization, which will be able to provide consumers" loyalty to the company's products, and their loyalty to the company itself, as well as to provide high long-term prospects of the business.

The third critical factor is a measure of short-term priorities of the investment cycle (8.1).

![This is a critical indicator of the investment cycle [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f081.jpg) - This is a critical indicator of the investment cycle.

- This is a critical indicator of the investment cycle.

Scheme: investment cycle: how it transforms company and makes it more prosperous

![Scheme: investment cycle: how it transforms company and makes it more prosperous [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s8.jpg)

As it can be seen from the scheme, namely the investment cycle changes the entire direction of the company"s development. This cycle is as if the company is re-created anew from time to time to become more technologically advanced, more competitive. And also that company would be able to carry a unique selling proposition to its customers, practically unique to the competition, a unique in satisfying customers' needs much more efficiently than the competitors" ways, so unique that it carries a more powerful information PR-shell, which creates a demand in society for goods of a company.

PPE (property, plant and equipment) acquisition should be significantly greater than PPE outflow, indicating that the modernization of the production process persists in the company. There is the problem within the domestic firms of PPE obsolescence, without mentioning the external, physical and other kinds of wear.

As a consequence, the production base of a company must continually develop to meet both modern Russian state of technology in an industry, and foreign experience, since it is no secret that the more and more new waves of more successful in financing activities global foreign and multinational companies come to Russian domestic market.

In addition, the forecast of what there is to be in the next 10 years or more - it is almost unreal. That is why the present dictates the need to continually update the material and manufacturing base for the Russian companies.

If a company does not follow this algorithm, the present is so, that even if it is successful, even when receiving profits (and this is one of the best variants for development of the situation); - this is due to the onset of the aristocratization stage from the theory of catastrophism. This stage involves a conservative financial strategy and the lack of large investments in permanent "rebirth" to the new technological and moral level (of the fashion, style, modernity, .....).

If there are no large investments - there are no big spending .... Hence, it is a hidden stage of the internal crisis in the company, since the development is not happening. However, in compensation, such company receives a windfall.

During this time the competition is improving and the company is rapidly being "left out" of development. Usually this means a gradual decline in sales, therefore, problems with production, overstocking, and then with Cash ... ..

Well, what is next - I think that you know it by yourself! It is this state of "temporary idyll", named Aristocratization by Adizes (Adizes, 1989, 1998), the state which ruined at the time, and promptly ruined, Mr. Adnan Khashoggi who was a multimillionaire, and who in less than 10 years lost, perhaps, more than $ 70 billion due to the fact that he missed this point....

You, dear reader, probably, now ask me, what is the hierarchy of all these cycles? The hierarchy is as follows. The most pressing problems for the company are prepared by this financial cycle as it rotates financial resources, and this is where the problem starts with the solvency of the business.

Second in the hierarchy is the marketing and the associated operational (production) cycle. This cycle - is a basis of generating cash income for the company.

And the third most important is the investment cycle, which should provide the company's prosperity in the long run.

The following factors are no longer critical, and they show the urgent problems of the company in all three cycles. We begin with the most critical cycle, financial. There raises the following figure (9):

![An indicator of the urgent problems in the financial cycle [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f9.jpg) - An indicator of the urgent problems in the financial cycle

- An indicator of the urgent problems in the financial cycle

Ideally, a company must have enough net income to cover all emerging payments on debt, both short-and long-term for payments averaged appearing in a certain year. That is why the denominator of this formula is the sum of short-term loans plus averaged index of imputed payments on long-term debt.

If the value of (9) is less than 1, it indicates a high probability of the presence of urgent problems in the financial cycle. This means that a company needs to work through risk management strategies in the management aspect of financial flows in case of abrupt changes of the bifurcation shifts in the financial environment.

The rate of company"s business activity should be analyzed to understand what is happening.

If business activity is high, then it may indicate high-risk activities of the company, which imposes itself on the need for risk management strategies, for example - the creation of reserves.

In any case, such companies are likely not to innovations. Such a company should identify high-risk illiquid assets and sell it from turnover to extinguish the debt, such companies need to build up reserves, to seek subordinated partners for the future, to conduct stress tests and so on.

The recipe here is one: to segment all the activities of the company for cash flow and to manage them!

To ensure that you could easily segment the company's activities for cash flows, the author of this paper will offer you, my dear reader, the following scheme.

![To ensure that you could easily segment the company's activities for cash flows, the author of this paper will offer you, my dear reader, the following scheme. [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s9.jpg)

Denotations in the scheme are as follows .

This matrix will let to analyze the performance of both Russian and foreign companies, dividing their business activity on the set of cash flows. Black markers in the scheme indicate paired indicators of cash flows.

In case of problems in this cycle, it is necessary to segment your company's activities for such cash flows and to analyze it. Now, let's figure of urgent problems in the operational and marketing cycle of the company (10):

![An indicator of the urgent problems in the operational and marketing cycles [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f10.jpg) - An indicator of the urgent problems in the operational and marketing cycles

- An indicator of the urgent problems in the operational and marketing cycles

Ideally, production and sales must be placed in the company so that the amount of revenue could cover the amount of current assets, that is, that figure (10) would be greater than or equal to 1. This suggests that the production is well-functioning, and the marketing is well-organized.

If it is not so, then there are some pressing problems in the cycle associated with a slowing of business turnover.

If the specified delay occurs, the company, if it is connected with the normal functioning, is necessary to create, possibly, non-core subsidiary company in industries and sectors that are able to provide constant revenue. That is, companies need to consider the feasibility of introducing new products, they need to find new markets and customers. Also they need to control production in order to minimize the amount of current assets, primarily receivables and inventories, including the amount of finished products.

All this can be done only through a successful marketing organization.

Therefore, please see the section of the financial analysis of the marketing plan in the other publications of the author. We now consider the following measure of the current problems in the investment cycle (11):

![An indicator of the urgent problems in the investment cycle [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f11.jpg) - An indicator of the urgent problems in the investment cycle

- An indicator of the urgent problems in the investment cycle

It so worldwide - a staff is considered as the foundation of any company ...

The following argument served as Pretext. It concerned the fact that there are industrial super-companies that are ready to get out of their skin by means of aggressive marketing to increase their sales, hence, production.

These wisent-bisons of business, having a super financial power, super volumes of current and non-current assets - they are often not able to provide high margins above 8% per year, recalculated to IFRS standards! That's it!

And there are some companies who have to balance only a building, a handful of computers, and they were able, just for a few decades, to grow to super-corporations like Microsoft, Apple, Google, Yahoo, Facebook, ... .. They usually don"t have so many recourses on balance as those wisent-bisons of business. And their profits ... .. are phenomenal!

Is it a just people who are able to make out of ordinary houses and their own knowledge and skills, something considerably more than even the largest classic wisent-bisons of business among manufacturing companies.

People began to wonder how this should be considered - a positive effect on staff in the balance. It is still a hard question for a science today - how to estimate the HR?!

There is a point of view to consider HR as a part of company"s overall goodwill. Today it is widely considered to reflect goodwill on balance of those operations that come from business-combinatorics (for example, acquisitions).

Goodwill - is an intangible asset, the difference between the actual market value of the company and how much it costs on the balance sheet. Some companies try to estimate the full value of goodwill in their internal financial analysis.

The companies that rely on the knowledge and skills of staff possess the largest financial goodwill, ie, companies of services (creating the software, support information flow, educational institutions, private upscale clinic (people travel to the U.S. clinics from the around the world on a very much fee basis), financial consulting, legal consulting, including major notary network, and so on).

In fact, these companies are selling ... the knowledge and skills of their employees, their interest in working for this company, that is, knowledge and skills of staff in conjunction with the corporate culture.

In fact, such companies very rarely do the material production, and they are able to give odds to industrial wisent-bisons of business!

Currently, conventionally, all companies are generally classified as mechanistic or organic, depending on how wide the intellectual potential of the staff is used. To learn the difference between a mechanistic organization from an organic one - you can learn it from the literature on corporate culture.

In short, the mechanistic culture - is a classic bureaucratic structure with a horizontal system of command and execution of orders, and sometimes it holds the departments of coordination and strategic business units, that operate relatively independently of the structure as a whole, and are subjects only to the top of the power of this type.

Personality in this structure is respected, at the same time, the organizational culture is not particularly stimulating creativity and ingenuity of workers. Where it is necessary, the mechanistic type of culture may be optimal. At the same time, it is not fair for the post-industrial companies.

Organic culture is characterized by companies with a corporate culture in the best traditions of models of Peters-Waterman and Sashe. That is, decisions are made jointly with the employees, there is a promotion of openness/closeness of communications, the principle of collective perception of a positive organizational environment, it encourages risky actions of employees within their competence and knowledge, and so on. All this must be based on faith inside the company and the activities of its employees.

The world today has about 78% of large companies that have a mechanistic type and 22% - organic.

There are some other non-Maneggiare approaches (from the old. Italian. Maneggiare-"Get in the hand (tool)" and the old. Lat. Manus - "The Hand"), that are not related to marketing and management; these are the approaches that try to make an interpretation of the success of postmodern companies in comparison with classical multinational and global corporations.

And now, let"s go back to our consideration of the indicator.

Staff - is a long-term key to success for any company. Nothing hurts the company as much as the retirement of staff. Staff is one of the most important guarantees of prosperity of any company. Because of this fact, the number of employees must not decrease itself, otherwise, it should be mentioned, it testifies about the possibility of internal crisis inside the company - it testifies about that fact that company can"t attract and retain the employees by its corporate culture, and so they may go to a competitor of such company, or, at best, to other sectors (that may also indirectly hurt the company).

In the case of staff decreasing as a result of lack of competence - it is better to replace it with a more suitable personnel because it determines the success of the company and its revenues in the long term, as well as an investment perspective. Investments in personnel - this is usually a long-lasting investment.

Now, let's look at all three cycles: the operational and marketing, investment and financial - let's look at all three cycles from the standpoint of long-term strategic prospects of the business-systems (12):

![An indicator of long-term risks in the financial cycle of the firm [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f12.jpg) - An indicator of long-term risks in the financial cycle of the firm

- An indicator of long-term risks in the financial cycle of the firm

If net income is not enough to cover the average arithmetically weighted amount of borrowed funds, then this indicates the presence of risk problems in the financial cycle. These problems should be resolved if time is on their resolution....

In this case, you should use the precious time to increase sales, perhaps, in new markets. You should also seek out and sell illiquid assets, reduce production costs by its components, to seek subordinated partners and so on.

Everything should be directed to the alignment of the company's market in the future, or to prepare the company to bankruptcy with minimal losses in the future. As well as in the previous case, we should pay attention to the partitioning of the company"s activity to cash flows for company"s best advantage, as it is shown in the scheme, which I have already given.

In this case, you must decide whether to continue funding the company will likely lead to the modernization of production and bring the company to a new production level. Or it will likely lead to even more compelled taking of additional loans to fill the financial gaps. Consequently, then over and over again, once more, again and again - and as long - until you do not stop or turn into a "minus millionaire" (a person with the amount in his or her accounts of 1 million or more, with a minus sign and actual numeral value). In general, this is the way which all the bankrupt-companies follow until their stop - so, it is important to answer this question fair.

If there is a sense of something better - you should do it quickly.

Otherwise - you need to minimize losses and to maximize the output to prepare the company for leaving the market in the future in the most secure way possible.

In principle, the critical indicators that show whether your company is able to cover its debts are the following:

![In principle, the critical indicators that show whether your company is able to cover its debts are the following: [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f13_15.jpg)

If these values are more than 1 - this is normal. If are not more than 1 - this is not normal! The coefficients show whether the cash from the sale of your goods is enough to pay debts, or the company will have to use non-continuous operations and/or have to take more loans .... then more ... more ... and more again....

Of course, such figures may be caused by the temporary crisis changes in the environment. Even in this case, it shows that your company is exposed to them. The work with these risks should be a priority.

However, we do not take the revenue - we take profit as an indicator that something should be done. It shows the direction in which a firm should dig in the future to avoid problems and to maximize its effectiveness ....

Now, let's look at the problems associated with operating and marketing cycles over the long term (16):

![This is a measure of the normal state of operational and marketing cycles in the long run [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f16.jpg) - This is a measure of the normal state of operational and marketing cycles in the long run.

- This is a measure of the normal state of operational and marketing cycles in the long run.

It shows that companies have enough revenue from main activities enough to cover the current assets and there is a reserve equal to the total value of stock material for the production and sales, which are calculated like one more time, like covering the reserve.

If the ratio is less than 1, it is necessary to improve production technology and production lines on which there is still enough time.

Indicator of long-term investment cycle in the normal state is as follows (17):

![An indicator of the normal state of the investment cycle [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f17.jpg) - An indicator of the normal state of the investment cycle

- An indicator of the normal state of the investment cycle

Remember, dear reader, we spoke with you about the importance of human resources? So, it is necessary that the staff turnover was minimal for to ensure long-term prosperity of the company and the normalization of the investment cycle. It should be so even with influx of workforce. That is why a personnel should be selected especially carefully.

This does not mean that you can"t dismiss - not at all! If you had many to dismiss, therefore, the personnel policy of the company is poor and needs to be more effective, because originally it was necessary to select the workforce corresponding to a specific of a company.

Also note that one should take the time to calculate the determinant of the resulting matrix (table) of Rapid analysis of the company. Determinant - is a mathematical component, geometric and graphical meaning of which is the volume of a polygon described by the matrix. So, the determinant of this matrix, it is desirable, should not be greater than 0 with five characters after the comma, that is, the graphic standard deviation of the risk should not be folded. The determinant of this matrix system is considered to be in accordance with the following scheme :

Scheme: Calculation of the determinant of the matrix system of indicators" rapid analysis

![Scheme: Calculation of the determinant of the matrix system of indicators’ rapid analysis [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s10.jpg)

To learn how to quickly calculate this matrix without any formulas - see the note .

I think many of you are familiar with Sudoku, the Japanese crossword puzzles. So, the matrix - this is a very similar thing! In general, we will return to the matrices, when it comes to financial analysis of portfolio of securities. There's matrix analysis to evaluate the optimal portfolio. Also, you and I will build an optimization model of the firm, based on matrix analysis, developed by the author of this paper. And there are much more complex matrixes to be calculated, that is why we shall not spend time for their calculation - we will use software means. I think, all of you have an Excel?! If not, then you can do it later on the computer when you will have such an opportunity. In the meantime, take, at least, a pencil, notepad and calculator - this is for now enough, so you can learn all the financial analysis in a very good volume.

Determinant of the matrix in this express-analysis model should be obtained and comply with five zeros (+ / - 0.00000).

Also, this model allows us to predict what will happen to your company, if nothing would be taken, within how many years it will most likely come from the market. This matrix and this model were developed by Alexander Shemetev, who is the author of this paper. The model of this calculation is shown at the diagram below :

![The model of this calculation is shown at the diagram below [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/s11.jpg)

Thus, the formula for calculating the company"s risk reserve is the following:

![Thus, the formula for calculating the company’s risk reserve is the following: [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f18.jpg) (18)

(18)

The end result, resulting in this formula, will show you what risky reserve your firm actually has. Reserve appears only when the value of the formula is above 1. This formula allows us to calculate the reserve of resources" availability to raise the capacity of the investment cycle.

If the ratio is obtained by less than 1, then the inclusion of company resources in the investment cycle can be irrational.

The calculation of the actual reserve should be made by the following formula:

![The calculation of the actual reserve should be made by the following formula: [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f19.jpg) (19)

(19)

Deficit shows how much money the company would be forced to cover the expense of third-party financing sources in a normalized manner. The deficit in more detail I together with you will look a bit later.

This model also allows to calculate the period of risks" focus, which can in the shortest possible time to take the company off the market. This risks" focus is the financial cycle functioning abruption risks" concentration for company, therefore, it is also connected with the investment and operational cycles.

The advent of risk can be considered through the focus of two formulas: the total life cycle of the company and methodology for calculating the critical point of termination of cash flows. This concentration of risks comes in, if not to prompt the up-to-time anti-crisis policy of the company's financial, operational, marketing or investment cycle.

Calculation of the onset of the maximum concentration of risks in the method of determining the risks" concentration point of the life cycle termination will be calculated in accordance with the following matrix, developed by the author of this paper:

Risky streams cycles" and risk components" rates decomposition matrix

![Risky streams cycles’ and risk components’ rates decomposition matrix [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/rsc.jpg)

The formula to calculate the total concentration of risks, which will show how much the company will have time in the event of a crisis dynamic of external environment is presented below:

![<img src=f20.jpg> [Alexander Shemetev]](/img/s/shemetew_a_a/alexandershemetevsmodelsforcomprehensivefinancialanalysis/f20.jpg) ** (20)

** (20)

This formula will allow you, my dear reader, to analyze any company from the inside and find out how much there will be time in the event of continuation of crisis trend dynamics in the external environment, that is, if the market and the economy situation do not change in favor of the analyzed companies.

For example, if the coefficient A has turned 0.6, the coefficient B - 0.4; C - 0,5; D - 0,7; E - 1,2; F - 0,9 for a company, if the external environment crisis development trends will be dominated at the market, it will have only 1.55 years for the implementation of anti-crisis policy.

However, in Russian conditions, you should always bear in mind exactly who is an observer of risk trends. This technique is designed to analyze the company from the inside. In Russia, one should take into account the fact that the accounting and financial-accounting may differ, including, for purposes of tax optimization. Therefore, to calculate the third-party organization one should use a different model, which we with you, dear reader, will look on.

Methods of calculating the critical point of termination of cash flows

This technique also developed by the author of this paper, Alexander Shemetev. It assumes that the actual concentration of risks, that are sufficient for termination of the company, comes not so much by the loss of the possibility of self-sustaining itself at the expense of normal activity in the market that was calculated by earlier methods; the next situation is taken into account: that later, a company would likely attract a critical mass of borrowed resources due to its lack of effectiveness, which could serve as a strong impetus to the bankruptcy of a business-system. This technique will allow you, my dear reader, to know when that moment happens for a specific company.

(0.1)

(1)

- This is a critical factor of the financial cycle (7)

- This is a critical indicator of risk concentrations of two cycles (8)

- This is a critical indicator of the investment cycle.

- An indicator of the urgent problems in the financial cycle

- An indicator of the urgent problems in the operational and marketing cycles

- An indicator of the urgent problems in the investment cycle

- An indicator of long-term risks in the financial cycle of the firm

- This is a measure of the normal state of operational and marketing cycles in the long run.

- An indicator of the normal state of the investment cycle

(18)

(19)

** (20)